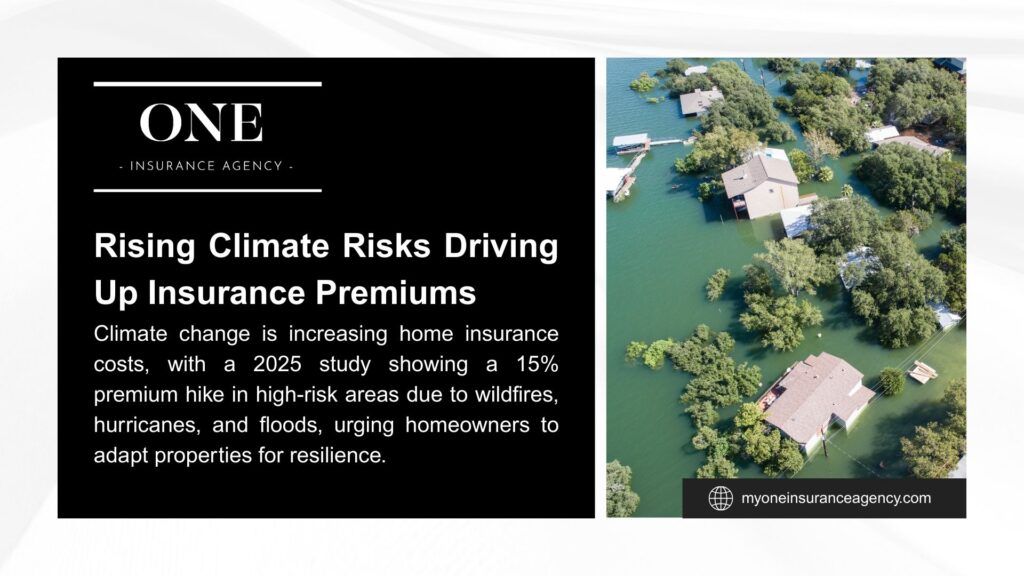

According to a 2025 LendingTree analysis, home insurance rates have jumped 40.4% over the past six years, with the average American homeowner now paying $2,801 annually. That’s a massive increase that’s hitting families hard across the country.

This Article Will Help You Learn:

- How much does home insurance cost in the United States

- What your policy actually covers (and what is not covered)

- How to determine the coverage amount that is right for you

- Why is there such variation in costs between states

- Smart ways to lower your premium

Average Home Insurance Costs by State (2025)

Here are the average home insurance costs from the 50 states of USA, according to NerdWallet recent analysis:

| State | Average Annual Cost | Average Monthly Cost |

| Alabama | $3,420 | $285 |

| Alaska | $1,035 | $86 |

| Arizona | $2,565 | $214 |

| Arkansas | $3,215 | $268 |

| California | $1,335 | $111 |

| Colorado | $4,175 | $348 |

| Connecticut | $1,870 | $156 |

| Delaware | $1,025 | $85 |

| Florida | $2,625 | $219 |

| Georgia | $2,435 | $203 |

| Hawaii | $610 | $51 |

| Idaho | $1,460 | $122 |

| Illinois | $2,420 | $202 |

| Indiana | $2,495 | $208 |

| Iowa | $2,505 | $209 |

| Kansas | $3,735 | $311 |

| Kentucky | $2,510 | $209 |

| Louisiana | $2,220 | $185 |

| Maine | $1,180 | $98 |

| Maryland | $1,945 | $162 |

| Massachusetts | $1,595 | $133 |

| Michigan | $2,095 | $175 |

| Minnesota | $2,920 | $243 |

| Mississippi | $3,310 | $276 |

| Missouri | $3,290 | $274 |

| Montana | $2,735 | $228 |

| Nebraska | $4,505 | $375 |

| Nevada | $1,305 | $109 |

| New Hampshire | $1,185 | $99 |

| New Jersey | $1,290 | $108 |

| New Mexico | $1,730 | $144 |

| New York | $1,740 | $145 |

| North Carolina | $2,490 | $208 |

| North Dakota | $2,805 | $234 |

| Ohio | $1,590 | $133 |

| Oklahoma | $6,210 | $518 |

| Oregon | $1,305 | $109 |

| Pennsylvania | $1,440 | $120 |

| Rhode Island | $2,080 | $173 |

| South Carolina | $2,225 | $185 |

| South Dakota | $2,350 | $196 |

| Tennessee | $3,345 | $279 |

| Texas | $4,585 | $382 |

| Utah | $1,385 | $115 |

| Vermont | $950 | $79 |

| Virginia | $1,705 | $142 |

| Washington | $1,415 | $118 |

| West Virginia | $1,770 | $148 |

| Wisconsin | $1,515 | $126 |

| Wyoming | $1,555 | $130 |

The 5 Most Expensive States for Home Insurance

If you live in these states, you are paying way more than the national average.

- 1. Oklahoma – $518/month ($6,210/year)

- 2. Colorado – $348/month ($4,175/year)

- 3. Kansas – $311/month ($3,735/year)

- 4. Texas – $382/month ($4,585/year)

- 5. Nebraska – $375/month ($4,505/year)

The 5 Cheapest States for Home Insurance

- 1. Hawaii – $51/month ($610/year)

- 2. Delaware – $85/month ($1,025/year)

- 3. Vermont – $79/month ($950/year)

- 4. Alaska – $86/month ($1,035/year)

- 5. New Hampshire – $99/month ($1,185/year)

What Does Home Insurance Cover?

1. Dwelling Coverage

| Covered Damage | Not Covered |

| Storm damage | Flood damage |

| Fire | Earthquake |

| Theft/vandalism | Normal wear |

| Falling objects | Poor maintenance |

| Lightning strikes | Termites/pests |

2. Personal Property Coverage

Your homeowner’s policy covers your possessions inside the home through personal property coverage – that is, your furniture, clothes, electronics, appliances, and personal items, in the event they become damaged or stolen.

3. Liability Protection

Liability coverage is the part of your policy that protects you financially should someone get injured on your property or you accidentally damage someone else’s property.

This coverage pays for their medical expenses, legal fees if they sue you, and any ensuing settlement costs, up to your policy limit.

4. Additional Living Expenses (Loss of Use)

When your home becomes impossible to live in after covered damage like a fire or major storm, this coverage helps pay for your temporary living costs while repairs are being made.

5. Other Structures Coverage

Your property probably has more than just your main house on it. Other structures’ coverage protects these additional buildings and features – detached garages, tool sheds, fences, driveways, and even in-ground swimming pools that aren’t attached to your main home.

6. Medical Payments Coverage

Medical payments coverage is a small but useful part of your policy that pays medical bills if a guest gets injured on your property, regardless of who was at fault. It’s designed for minor injuries to be handled quickly without lawsuits or establishing blame.

How Much Home Insurance Do You Really Need?

It is very important for you to get the right coverage because too little insurance can leave you financially unstable after a disaster and too much insurance can make you overpay every year.

- Dwelling Coverage (Your House)

Don’t base your coverage on what you paid for the home or what it’s worth today. You need enough insurance to completely rebuild your house from the ground up if it’s destroyed.

How to estimate it:

- Ask a local contractor how much it costs to build per square foot in your area.

- Multiply that by your home’s total square footage.

- Add 10% to cover rising labor and material costs.

Example: 2,000 sq ft × $150/sq ft = $300,000 in dwelling coverage needed

- Personal Property Coverage (Your Stuff)

Most people own a lot more than they realize, and the best way to make sure everything is covered is to record a quick walkthrough video of your house.

Average value of personal items:

- Bedroom: $15,000–$25,000

- Living Room: $10,000–$20,000

- Kitchen: $5,000–$15,000

Add up all your rooms. Most homeowners need at least $100,000 in personal property coverage.

You will need more coverage if you own expensive items such as jewelry, art or collections.

- Liability Coverage (Lawsuits)

The liability coverage is important because it protects you if someone gets hurt on your property or sues you. Start with a minimum of $300,000 in liability coverage, and if you have large assets, go for $500,000 or more.

- Loss of Use Coverage (Living Expenses)

If a fire or storm makes your home unlivable, this coverage helps you to pay for temporary housing, meals, and other extra costs.

To estimate:

- Monthly rent for a similar home in your area

- Extra costs from eating out

- Additional gas for a longer commute

- Storage unit fees

Multiply your estimate by 12 months, just to be safe. It is better to have more coverage than to run out halfway through repairs.

If you want to learn more about how much home insurance you really need, check out our article.

One Insurance Agency Is An Industry Leading Business For Home insurance

When it comes to protecting your home, ONE Insurance Agency has been rated as the #1 top leading independent broker by hundreds of homeowners.

They have helped families save thousands of dollars on bundled policies and protected small businesses with proper liability coverage.

Get your free consultation today and find coverage that actually fits your life and your budget.

Frequently Asked Questions From Homeowners

- Why is home insurance so expensive in Oklahoma?

The reason why Oklahoma has very expensive home insurance is that tornadoes and hailstorms cause major property damage frequently, which leads to higher insurance claims.

- Can I actually lower my home insurance bill?

Yes, definitely. Several ways to lower your house insurance bill are to increase your deductible, bundle your home and auto policies, improve your credit score, and install home security features

- Do I still need home insurance if my house is paid off?

If your house’s mortgage is paid off, legally, you are not required to have insurance. But it can be a major risk because some people cannot afford to rebuild their house if there is a fire or storm. So it is better to keep the coverage in place.

- Why Do I Need Flood Insurance?

If you live in places near seas or in a region that has heavy rainfalls frequently you should consider flood insurance. Please keep in mind that standard home insurance DOES NOT COVER flood damage!